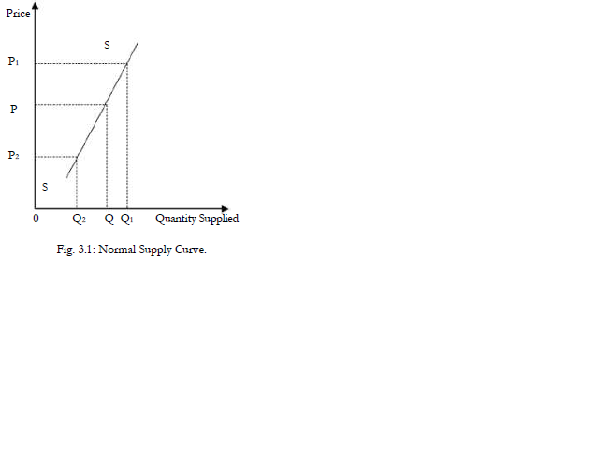

1. Ceteris paribus, supply is defined as the quantity of goods (and services) which producers (suppliers)

are willing and able to offer for sale at alternative prices per unit of time. Supply is an increasing function of (own) price such that more of a commodity is supplied at higher than at lower prices. This direct relationship between supply and own price of a commodity is represented by an upward sloping supply curve illustrated below:

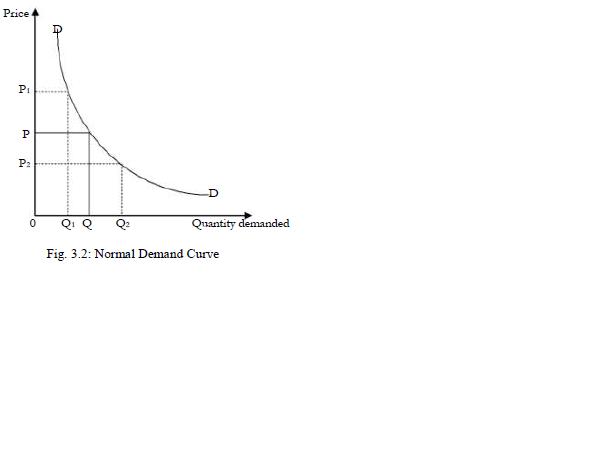

2. Demand is the quantity per unit of time which consumers (households) are willing and able to buy in the market at alternative prices. Demand is a decreasing function of (own) price such that more of a

commodity is demanded at lower than at higher prices. This inverse relationship between demand and own

price of a commodity is represented by a downward sloping demand curve as shown below:

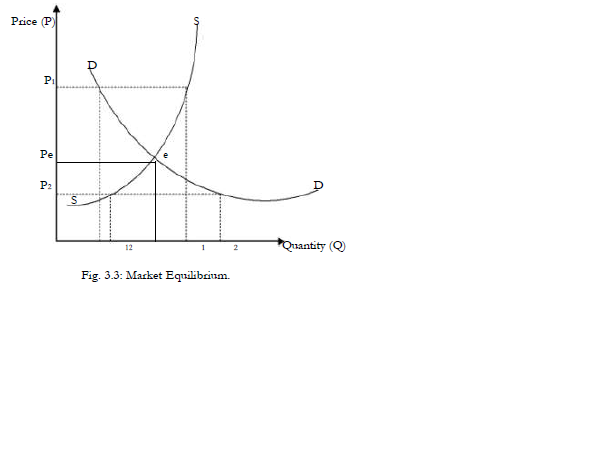

3. Equilibrium price is the market price determined by the free interaction of the market forces of supply and demand. Once this price level is achieved there is no tendency for it to change and the market clears. Equilibrium price is determined at the intersection point of the supply and demand curves (equilibrium point), such that the quantity of a commodity at this point is called the equilibrium quantity. The determination of the equilibrium price and quantity is diagrammatically demonstrated as shown below:

Pe is the equilibrium price and Qe the equilibrium quantity.

At the price P1 there is excess supply over demand represented by (Qs1 - Qd1) units which creates a downward pressure on price to fall in order for suppliers to dispose of the surplus.

At P2 there is excess demand over supply represented by (Qd2 – Qs2) units which results in an upward

pressure on price to increase.

Overall, the tendency is towards Pe and Qe, and any prices and quantities other than Pe and Qe are known as disequilibrium prices and quantities.

Wilfykil answered the question on

February 4, 2019 at 10:21