Industrial analysis

- Industrial analysis involve comparison of firm performance with the industrial

average performance or norms.

- This analysis can only be carried out for a given year. i.e

Times series/trend analysis

- This involve analysis of the performance of a given firm over time i.e ratio of

different year of a given Co. are compared in order to establish whether the

performance is improving or declining and in case a weakness is detected e.g

decline in liquidity ratio, this will force the management to take a corrective

action.

- When commenting on industrial and trend analysis the following 4 critical

points should be highlighted:

a) In case of individual ratio classify them in their immediate category e.g

when commenting on TIER indicate this in a gearing ratio.

When commenting on a given category of ratio identify the ratios in

that category e.g if required to comment on liquidity position identify

the liquidity ratio from the ratios computed.

b) State the observation made e.g total asset turnover is declining or

increasing over time (in case of trend analysis) or the ratio is lower or

higher than the industrial norms (in case of industrial analysis).

c) State the reason for observation i.e. explain why the ratio is declining

or increasing.

d) State the implication for observation e.g decline in liquidity ratio means

that the ability of the firm to meet in short term financial obligation is

declining over time.

Inventory turnover

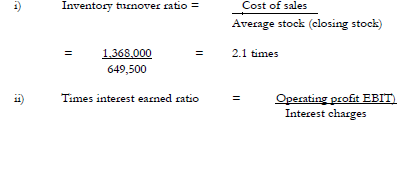

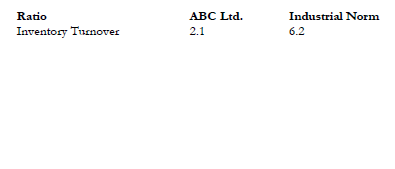

- This is a turnover or efficiency ratio

- The rate is lower than industrial norm

- A low stock turnover could be attributed to:

i) Charging higher price than competition

ii) Maintenance of slow moving/obsolete goods

iii) Where the firm is selling strictly on cash while

competitors are selling on credit.

- The firm is not efficiently utilizing its inventory to

generate sales revenue.

i i) Times interest earned ratio (TIER)

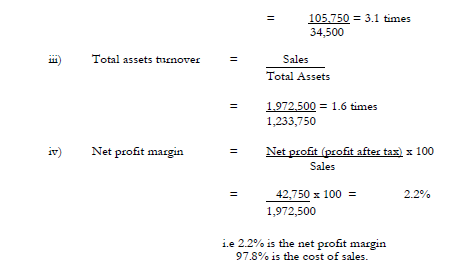

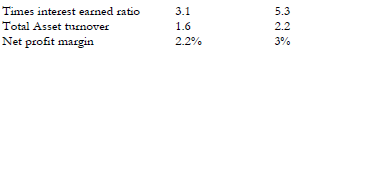

- This is a gearing ratio

- It is lower than industrial average or norm

- This could be due to low operating profit due to high

operating expenses or high interest charges due to

high level of gearing/debt capital.

- This implies that the firm is using a relatively high

level of fixed charge capital to finance the acquisition

of assets.

iii) Total asset turnover

- This is efficiency ratio/activity

- Lower than industrial average

- This could be due to holding large non-operational or

fully depreciated asset which are not utilized by the

firms.

- This implies inefficiency in utilization of total assets to

generate sales revenue.

Net profit margin

- Is a profitability ratio

- Lower than industrial norm

- This could be due to low level of net profit of the

firm relative to sales revenue.

- This implies that the firm has a low ability to control

its cost of sales, operating & financing expenses e.g in

case of ABC Ltd selling & admin expenses are equal

to 82.5% of gross profit

marto answered the question on

February 12, 2019 at 09:40