a) You are required to explain the controls that can be established over completeness of input

Controls over completeness of input seek to ensure that all input data is captured by the system for processing

-Use of batch totals where by the total input data processed is compared with the original batch totals;

- Use of document count edit control to verify where transactions are supported by pre-numbered documents that all the transactions are recorded by reference to the documents utilised.

- By investigating any data rejections to ensure that the reasons are established and where necessary the data resubmitted for processing;

- Manual comparison of input data to output to ensure that all transactions have been recorded;

- Use of hash totals. A hash total is a control total without a defined meaning, such as the total of employee numbers or invoice numbers, that is used to verify the completeness of data. Thus the hash total for the employee listing by the personnel department could be compared with the total generated during the payroll run;

- Use of record count edit control. This is a control total of the number of records processed during the operation of a program.

b) Controls over validity

These controls seek to ensure that only valid transactions are processed. The controls that management can put in place include: - Validity checks in the hardware. This consists of the hardware that transmits or receives data comparing the bits in each byte to the permissible combinations in order to determine whether they constitute a valid structure;

- Reasonableness tests which check the logical correctness of relationships among the values of data items on an input and the corresponding master file record. For example if employees work only for eight hours, a reasonableness test could

be performed to determine that no employee is credited with more than eight working hours. Such control will check for the validity of the input data;

- Validity checks- these are tests of identification numbers or transaction codes for validity by comparison with items already known to be correct or authorised. For example KRA PIN numbers can be compared with the PIN numbers in the personnel records

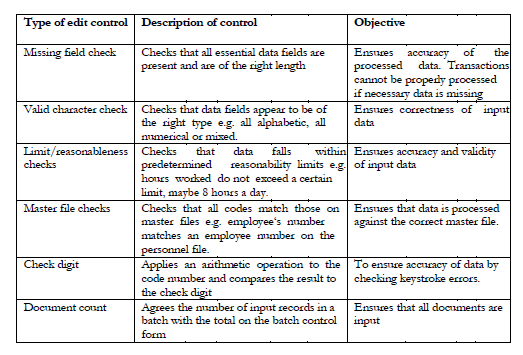

c) The most common input controls are edit controls. Examples of edit controls include;

Wilfykil answered the question on

February 21, 2019 at 07:47