1. Use of debt in the capital structure

- In Kenya as in many other countries, interest on cooperative debt is tax deductible companies can take maximum advantage of this tax deducting by determining the optimum amount of debt they can take and work with. It should be noted that the revenue authorities attempt to limit abuse of tax deductibility

- Section 16 (2i) of the income tax Act provides that interest on debt that is in excess of the thrice the shareholders equity of a company controlled by a non-resident in not tax deductible.

- The practice of over leveraging company with debt from associated sources so as to minimize taxable income. (known as thin capitalization) is well known and tax

- Authorities look out for it. Hence company’s working to take advantage of tax deducting should do so with the letter and spirit of income tax Act.

- Another technique for taking advantage of debts is the use of lease financing arrangement for the acquisition of assets rather than purchase with company’s fund as the lease payment made both capital and opportunity leases are tax deductible on the leases.

2. Capital investment allowances

The income tax act enables companies to change against their income certain allowance on capital expenditure. These allowances include wear and tear allowances for fixed assets on capital expenditure. These are covered under section 15 (2) and the 2nd schedule of the income tax act. These allowances serve as investment incentives Notable there is an investment deduction of 10% on industrial buildings used for manufacture as well as hotels constructed from 1st January 2004

3. Write off of bad trade debts and inventory and changing other allowable deductions

Section 15 (2a) of the income tax act allows the tax deductible on write off of bad debts subject to the approval of the commissioner. The commissioner is in the process of developing guidelines for the write off of bad debts within a period of 2 years after the expiry of 3 years since the bad debts came into existence.

Further VAT payable is given by the difference between output tax and input tax and since it is payable by the 20th of the due dates. This is more advantageous in case of large tax payers

Inventory writes off as effective or absolute is similarly tax deductible

There are write off as effective deduction detailed in the income tax Act which will enable business to reduce their taxable income if they actually utilize them. VAT should ensure that they source from supplies that will change VAT. That way the business buying can deduct input VAT from their output VAT and lower tax payable. While this is a matter well established in much business many other especially small and medium sized enterprises do not do this.

Another way of mitigating the tax burden is by importing from tax advantaged countries. This entails importing from within the East African community or the COMESA. These areas will eventually become free trade enabling duty free imports within them.

4. Export processing zones

Business where principal markets are foreign can set up a licensed export processing zones and enjoy a rating of tax incentives.

This include a 10 year tax holiday and modest 25% for the next 10 years exemptions from withholding taxes on dividends and other payments to non-residents for the first 10 years exemptions from VAT and investment deduction of 100 %

It should however be noted that sales within the EAC do not constitute exports for this purpose.

5. Off share business structure

The sparse collection of double taxation treaties to which Kenya is a party subjects international business and investment to multiple taxes on the same income.

- In practice, few business take advantage of the tax credit scheme under sec 42 of the income tax act which many multinational simply taking foreign taxes paid as a tax deductible business expense.

- Business can mitigate their tax burden on off share investment by establishing off share investment specifically in countries with relatively lower taxes or that could even be tax free i.e. tax havens such jurisdiction include Mauritius, Hongkong, Dubai etc

- The benefit of establishment in such jurisdiction is that they have a broad network of durable taxation and or relatively lower tax rates on income whenever it is generated or accrues.

Wilfykil answered the question on February 25, 2019 at 12:24

- What techniques or ways can individuals take advantage of to avoid taxes?(Solved)

What techniques or ways can individuals take advantage of to avoid taxes?

Date posted: February 25, 2019. Answers (1)

- Tax refunds and tax credits are increasingly being used by governments in the information and modernization taxation policies(Solved)

Tax refunds and tax credits are increasingly being used by governments in the information and modernization taxation policies.

Required:

i) Citing examples distinguish between a tax refund” and a “tax credit”

ii) Evaluate the fundamental role of tax refunds and tax credits in a government’s developments agenda

Date posted: February 25, 2019. Answers (1)

- In the year ended 31 December 2011. Malipo Ltd. earned a profit before tax of Sh. 400 million from its main operation.(Solved)

In the year ended 31 December 2011. Malipo Ltd. earned a profit before tax of Sh. 400 million from its main operation.

In addition, the company earned an investment income of Sh. k60 million. Dividend paid to members for the year amounted to Sh. 98 million.

The corporation tax rate is 30%

Required:

Shortfall tax, inclusive of penalties (if any) payable by the company for the year ended 31 December 2011.

Date posted: February 25, 2019. Answers (1)

- Justify the imposition of shortfall tax on companies(Solved)

Justify the imposition of shortfall tax on companies

Date posted: February 25, 2019. Answers (1)

- A number of countries, particularly in the developing world, have rest fact urea their revenue authorities to provide for large taxpayer units (LTUs).(Solved)

A number of countries, particularly in the developing world, have rest fact urea their revenue authorities to provide for large taxpayer units (LTUs).

Required;

i) Explain three reasons that have motivated the formation of LTUs.

ii) As a tax consultant in a country that intends to form an LTU, describe three key functional areas of an LTU.

Date posted: February 25, 2019. Answers (1)

- Discuss three reasons that related parties may give to justify the continued use of transfer pricing systems.(Solved)

Discuss three reasons that related parties may give to justify the continued use of transfer pricing systems.

Date posted: February 25, 2019. Answers (1)

- Describe ways in which related parties could be transfer pricing systems to avoid tax(Solved)

Describe ways in which related parties could be transfer pricing systems to avoid tax

Date posted: February 25, 2019. Answers (1)

- Briefly explain how firms or individuals could mitigate tax exposure through.

i) Stock dividends

ii) Share repurchases programmes.

iii) Registered venture capital entities.(Solved)

Briefly explain how firms or individuals could mitigate tax exposure through.

i) Stock dividends

ii) Share repurchases programmes.

iii) Registered venture capital entities.

Date posted: February 25, 2019. Answers (1)

- Discuss four tax incentives that could "have contributed to the growth of financial markets in your country.(Solved)

Discuss four tax incentives that could "have contributed to the growth of financial markets in your country.

Date posted: February 25, 2019. Answers (1)

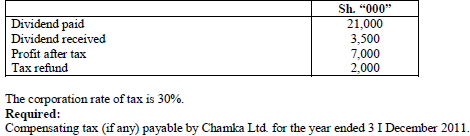

- The following information was provided by Chamka Ltd. for the year ended 31 December 2011.(Solved)

The following information was provided by Chamka Ltd. for the year ended 31 December 2011.

Date posted: February 25, 2019. Answers (1)

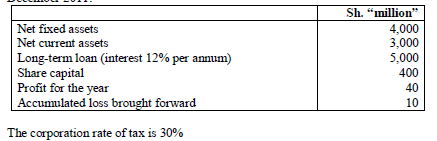

- Savana Holdings Ltd. is a foreign controlled company operating in your country.

The following information was extracted from the financial statements for the year ended 31...(Solved)

Savana Holdings Ltd. is a foreign controlled company operating in your country.

The following information was extracted from the financial statements for the year ended 31 December 2011:

Required:

i) Justify the argument that the company was thinly capitalized.

ii) Compute the company's interest tax shield.

Date posted: February 25, 2019. Answers (1)

- Mr. Maji Mengi knows very little about double taxation agreements. He is a consultant, who works in many countries and in many cases, he has...(Solved)

Mr. Maji Mengi knows very little about double taxation agreements. He is a consultant, who works in many countries and in many cases, he has ended up paying taxes on the same income more than once.

Required:

Explain to Mr. Maji Mengi the concept of double taxation treaty.

Date posted: February 25, 2019. Answers (1)

- Having read in the press about the benefits accruing to Kenya businessmen as a result of regional initiatives such as the East African Community and...(Solved)

Having read in the press about the benefits accruing to Kenya businessmen as a result of regional initiatives such as the East African Community and COMESA, Mr. Jitendra Kumar, a prominent foreign businessman has contacted you seeking your advice on how he could reduce his liability to tax arising from expansion of his business operations into Kenya

Required:

A report addressing in clear and concise details, the following matters raised by Mr. Jitendra Kumar.

(a) The tax objectives under the COMESA treaty.

(b) Rules of origin provisions under the COMESA treaty.

Date posted: February 25, 2019. Answers (1)

- Kenya has entered into double taxation agreements with a number of countries. Explain the meaning and implications of a double taxation relief.(Solved)

Kenya has entered into double taxation agreements with a number of countries. Explain the meaning and implications of a double taxation relief.

Date posted: February 25, 2019. Answers (1)

- Outline the benefits which may accrue to a country from being a signatory to the most favored nation's status agreement(Solved)

Outline the benefits which may accrue to a country from being a signatory to the most favored nation's status agreement

Date posted: February 25, 2019. Answers (1)

- Daniel Otwori, a resident of Kenya earned income from the countries listed below during the year ended 31 December 2006. Income from Kenya: ksh 1,765,000(Solved)

Daniel Otwori, a resident of Kenya earned income from the countries listed below during the year ended 31 December 2006. Income from Kenya: ksh 1,765,000

Income from United Kingdom (UK) UK £4,800 net Tax deducted amounted to UK £960. The average exchange rate during the year was 1 UK £ = 140 KSH, .A double taxation agreement exists between Kenya and United Kingdom.

Required:

The double taxation relief (in Kenya shillings) due to Daniel Otwori for the year ended 31 December 2006.

Date posted: February 25, 2019. Answers (1)

- A few countries and regions in the world have established themselves as tax havens. However, the anticipated inflow of investments has not been as high...(Solved)

A few countries and regions in the world have established themselves as tax havens. However, the anticipated inflow of investments has not been as high as expected by these countries and regions:

Required:

i. Briefly describe the concept of ‘tax havens’

ii. Summarize three benefits that might accrue to an investor in a tax haven

Date posted: February 25, 2019. Answers (1)

- Hodari Nkan is resident of Kenya. During the year ended 31 December 2010, he received the following income:(Solved)

Hodari Nkan is resident of Kenya. During the year ended 31 December 2010, he received the following income:

From Kenya: Sh. 720,000

From Zambia Sh. 540,000 (net of tax of sh. 78,000)

Assume that Kenya has a double taxation agreement with Zambia

Required:

The double taxation relief due to Hodari Nkan for the year ended 31 December 2010

Date posted: February 25, 2019. Answers (1)

- A generalized system of preference (GSP) applies where a country grants preferential treatment to goods and services received from another country.(Solved)

A generalized system of preference (GSP) applies where a country grants preferential treatment to goods and services received from another country.

Required:

Describe three general conditions to be fulfilled for goods or services from one country to benefit from a GSP.

Date posted: February 25, 2019. Answers (1)

- Explain how the tax legislation in your country attempts to prevent creative accounting by multinational companies(Solved)

Explain how the tax legislation in your country attempts to prevent creative accounting by multinational companies

Date posted: February 25, 2019. Answers (1)