An error may lead to understatement or overstatement of the tax liability. The tax payer has the responsibility of filling complete and accurate returns i.e. the installment tax returns and self assessment returns. If the error is discovered by the tax payer he can apply for relief or error or mistake. This must be done within a period of 7 years after the returns have been filed.

- If the commissioner agrees with the application he issues an amended assessment to the tax payer.

- If the commissioner does not agree with the application and take tax payer is not satisfied the tax payer can appeal to the local tax committee and then to the court of law.

- If the error is discovered by the commissioner he can issue an amendment statement. This can be amended either upwards or downwards.

- If is amended downwards it will lead to refund of tax to the tax payer. The amended assessment must be issued within a period of seven years.

Wilfykil answered the question on February 25, 2019 at 12:51

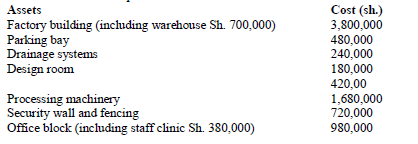

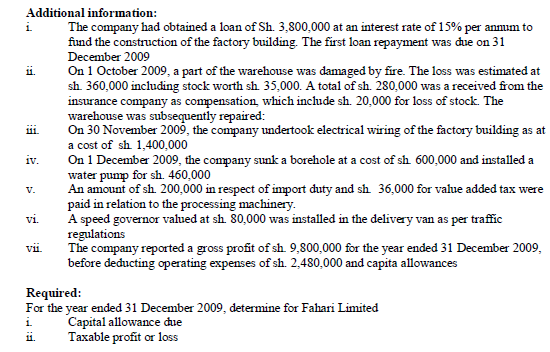

- Fahari Limited, a company making various leather products, commenced operation on 1 January 2009. The following information relate to the assets that the company purchased...(Solved)

Fahari Limited, a company making various leather products, commenced operation on 1 January 2009. The following information relate to the assets that the company purchased or constructed before commencement of operations

Date posted: February 25, 2019. Answers (1)

- What should individuals and corporates put in mind to mitigate their tax exposure or avoid being taxed unfairly?(Solved)

What should individuals and corporates put in mind to mitigate their tax exposure or avoid being taxed unfairly?

Date posted: February 25, 2019. Answers (1)

- How can corporates avoid taxes?(Solved)

How can corporates avoid taxes?

Date posted: February 25, 2019. Answers (1)

- What techniques or ways can individuals take advantage of to avoid taxes?(Solved)

What techniques or ways can individuals take advantage of to avoid taxes?

Date posted: February 25, 2019. Answers (1)

- Tax refunds and tax credits are increasingly being used by governments in the information and modernization taxation policies(Solved)

Tax refunds and tax credits are increasingly being used by governments in the information and modernization taxation policies.

Required:

i) Citing examples distinguish between a tax refund” and a “tax credit”

ii) Evaluate the fundamental role of tax refunds and tax credits in a government’s developments agenda

Date posted: February 25, 2019. Answers (1)

- In the year ended 31 December 2011. Malipo Ltd. earned a profit before tax of Sh. 400 million from its main operation.(Solved)

In the year ended 31 December 2011. Malipo Ltd. earned a profit before tax of Sh. 400 million from its main operation.

In addition, the company earned an investment income of Sh. k60 million. Dividend paid to members for the year amounted to Sh. 98 million.

The corporation tax rate is 30%

Required:

Shortfall tax, inclusive of penalties (if any) payable by the company for the year ended 31 December 2011.

Date posted: February 25, 2019. Answers (1)

- Justify the imposition of shortfall tax on companies(Solved)

Justify the imposition of shortfall tax on companies

Date posted: February 25, 2019. Answers (1)

- A number of countries, particularly in the developing world, have rest fact urea their revenue authorities to provide for large taxpayer units (LTUs).(Solved)

A number of countries, particularly in the developing world, have rest fact urea their revenue authorities to provide for large taxpayer units (LTUs).

Required;

i) Explain three reasons that have motivated the formation of LTUs.

ii) As a tax consultant in a country that intends to form an LTU, describe three key functional areas of an LTU.

Date posted: February 25, 2019. Answers (1)

- Discuss three reasons that related parties may give to justify the continued use of transfer pricing systems.(Solved)

Discuss three reasons that related parties may give to justify the continued use of transfer pricing systems.

Date posted: February 25, 2019. Answers (1)

- Describe ways in which related parties could be transfer pricing systems to avoid tax(Solved)

Describe ways in which related parties could be transfer pricing systems to avoid tax

Date posted: February 25, 2019. Answers (1)

- Briefly explain how firms or individuals could mitigate tax exposure through.

i) Stock dividends

ii) Share repurchases programmes.

iii) Registered venture capital entities.(Solved)

Briefly explain how firms or individuals could mitigate tax exposure through.

i) Stock dividends

ii) Share repurchases programmes.

iii) Registered venture capital entities.

Date posted: February 25, 2019. Answers (1)

- Discuss four tax incentives that could "have contributed to the growth of financial markets in your country.(Solved)

Discuss four tax incentives that could "have contributed to the growth of financial markets in your country.

Date posted: February 25, 2019. Answers (1)

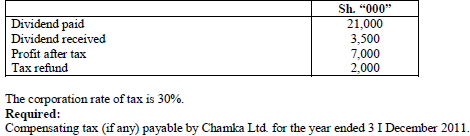

- The following information was provided by Chamka Ltd. for the year ended 31 December 2011.(Solved)

The following information was provided by Chamka Ltd. for the year ended 31 December 2011.

Date posted: February 25, 2019. Answers (1)

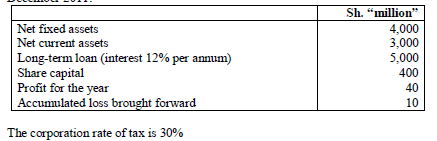

- Savana Holdings Ltd. is a foreign controlled company operating in your country.

The following information was extracted from the financial statements for the year ended 31...(Solved)

Savana Holdings Ltd. is a foreign controlled company operating in your country.

The following information was extracted from the financial statements for the year ended 31 December 2011:

Required:

i) Justify the argument that the company was thinly capitalized.

ii) Compute the company's interest tax shield.

Date posted: February 25, 2019. Answers (1)

- Mr. Maji Mengi knows very little about double taxation agreements. He is a consultant, who works in many countries and in many cases, he has...(Solved)

Mr. Maji Mengi knows very little about double taxation agreements. He is a consultant, who works in many countries and in many cases, he has ended up paying taxes on the same income more than once.

Required:

Explain to Mr. Maji Mengi the concept of double taxation treaty.

Date posted: February 25, 2019. Answers (1)

- Having read in the press about the benefits accruing to Kenya businessmen as a result of regional initiatives such as the East African Community and...(Solved)

Having read in the press about the benefits accruing to Kenya businessmen as a result of regional initiatives such as the East African Community and COMESA, Mr. Jitendra Kumar, a prominent foreign businessman has contacted you seeking your advice on how he could reduce his liability to tax arising from expansion of his business operations into Kenya

Required:

A report addressing in clear and concise details, the following matters raised by Mr. Jitendra Kumar.

(a) The tax objectives under the COMESA treaty.

(b) Rules of origin provisions under the COMESA treaty.

Date posted: February 25, 2019. Answers (1)

- Kenya has entered into double taxation agreements with a number of countries. Explain the meaning and implications of a double taxation relief.(Solved)

Kenya has entered into double taxation agreements with a number of countries. Explain the meaning and implications of a double taxation relief.

Date posted: February 25, 2019. Answers (1)

- Outline the benefits which may accrue to a country from being a signatory to the most favored nation's status agreement(Solved)

Outline the benefits which may accrue to a country from being a signatory to the most favored nation's status agreement

Date posted: February 25, 2019. Answers (1)

- Daniel Otwori, a resident of Kenya earned income from the countries listed below during the year ended 31 December 2006. Income from Kenya: ksh 1,765,000(Solved)

Daniel Otwori, a resident of Kenya earned income from the countries listed below during the year ended 31 December 2006. Income from Kenya: ksh 1,765,000

Income from United Kingdom (UK) UK £4,800 net Tax deducted amounted to UK £960. The average exchange rate during the year was 1 UK £ = 140 KSH, .A double taxation agreement exists between Kenya and United Kingdom.

Required:

The double taxation relief (in Kenya shillings) due to Daniel Otwori for the year ended 31 December 2006.

Date posted: February 25, 2019. Answers (1)

- A few countries and regions in the world have established themselves as tax havens. However, the anticipated inflow of investments has not been as high...(Solved)

A few countries and regions in the world have established themselves as tax havens. However, the anticipated inflow of investments has not been as high as expected by these countries and regions:

Required:

i. Briefly describe the concept of ‘tax havens’

ii. Summarize three benefits that might accrue to an investor in a tax haven

Date posted: February 25, 2019. Answers (1)