Methods used in adjusting transfer prices

1. Comparable uncontrolled price method (CUP)

CUP method corporate the price at which a comparable and uncontrolled transaction is conducted. Comparability between these transactions i.e. (controlled and uncontrolled) exist where there are no difference between transaction or if there is when such differences do not have a material effect or for which reasonable adjustment can be made hence an arm length transfer prices can be determined through a comparison with a sales price between 2 unreleased incorporations executing a comparable transaction. However the fact that virtually any minor differences in the circumstances of trade may have a significant effect on the price make it exceedingly difficult to find a transaction that are sufficiently comparable.

2. Cost plus method (CP)

This method is generally used for the trade of finished goods, it is determined by adding': an appropriate mark up to the costs incurred by the selling party in manufacturing or purchase the goods provided with the appropriate markup been based on the profits of other companies comparable to the involved parties. Cost based approaches are however not transparent as they appear. A company can easily manipulate its cost accounts to alter the magnitude of the transfer price.

3. Re-sale price method (RP)

This is found by working backwards from transactions taking place at the next stage in the supply chain and is determined by subtracting an appropriate gross mark-up from the sales price to an unrelated third party with the appropriate gross margin been determined by examining conditions under which the goods or services are sold and comparing the) said transactions to third party transactions.

4. Profit split method (PS)

This method is applied when the business involved in the examined transactions are too integrated to allow for separate evaluation and so the ultimate profit derived from the endeavor is split based on the level of contribution. It is often determined by some measurable factors such as employees' compensation. Payment of administration expenses of each participant in the project.

Wilfykil answered the question on February 26, 2019 at 05:39

- Explain the meaning of transfer pricing?(Solved)

Explain the meaning of transfer pricing?

Date posted: February 26, 2019. Answers (1)

- Kamere Ltd. commenced manufacturing operations on 1 January 2003. The management of the company has prepared the following financial statement for the year ended 31...(Solved)

Kamere Ltd. commenced manufacturing operations on 1 January 2003. The management of the company has prepared the following financial statement for the year ended 31 December 2005.

Balance sheet as at 31 December 2005

Additional information:

1. Non-current assets are stated net of depreciation including for year 2005. It is the policy of the company to charge depreciation at 20 % per annum on a straight line method.

2. The company has not claimed capital allowance since it commenced operations.

3. The company's reported taxable profits for the year ended 31 December 2003 and 2004 were sh.8,000,000 andsh.6,400,000 respectively

4. Factory building includes an extension to the factory constructed at a cost of sh. 1,600,000 which was put into use on I January

5. Machinery include generator and conveyor belts bought for sh. 1,400,000 and sh. 800,000 respectively.

6. Motor vehicles include a forklift purchased in 2003 at sh. 1,160,000.

7. A saloon car purchased in year 2004 at sh. 1,200,000 was disposed of during the year 2005 for sh. 600,000 no adjustment have been made to record this disposal.

8. The loan was received on 1 January 2005 and is subject to interest at the rate of 8% per annum

Required:

i) Capital allowances due to Kamere Ltd. for each of the three years ended 31 December 2003 , 2004, and 2005

ii) Adjusted taxable profit or loss for the company in each of the three years above.

Date posted: February 26, 2019. Answers (1)

- The Kenya Revenue Authority ("KRA") is geared towards a function-based organization rather than one structured along the types of taxes. This is evidenced by the...(Solved)

The Kenya Revenue Authority ("KRA") is geared towards a function-based organization rather than one structured along the types of taxes. This is evidenced by the integration of VAT, Income Tax and Excise departments into the Domestic Department. Asses the likely benefits and drawbacks to KRA arising from this integration

Date posted: February 26, 2019. Answers (1)

- Fruit farm Ltd. produces pineapple juice for sale in both local and export markets. The company owns plantations in Sagan which supply pineapples to the...(Solved)

Fruit farm Ltd. produces pineapple juice for sale in both local and export markets. The company owns plantations in Sagan which supply pineapples to the processing factory located in Thika.

The following is a summary of the company’s income statement for the year ended 31 December 2006.

Required:

i) Capital allowances due to Fruit farm Ltd. for the year ended 31 December 2006

ii) Adjusted taxable profit or loss for the year to 31 December 2006.

Date posted: February 26, 2019. Answers (1)

- The following information relates to ABC Ltd. for the year ended 31 December 2006.(Solved)

The following information relates to ABC Ltd. for the year ended 31 December 2006.

- Profit before tax sh. 4,000,000

- Import duty refunded by the authority sh. 400,000

- Dividend distributed by .ABC Ltd. sh. 8,800,000

- Dividend distributed by ABC Ltd. Sh. 3,000,000

- Corporation tax rate 30%.

Required:

Compensating tax payable by ABC Ltd. for the year ended 31 December 2006.

Date posted: February 26, 2019. Answers (1)

- The following information was extracted from the books of Faida Ltd. for the year ended 31 December 2006(Solved)

The following information was extracted from the books of Faida Ltd. for the year ended 31 December 2006

- Profit before tax sh. 400,000

- Import duty refunded by tax authority sh. 400,000

- Dividend distributed by Faida Ltd. sh. 8,800,000.

- Dividend received by Faida Ltd. sh 3,000,000

The rate of corporation tax is 30%

Required:

Compensating tax payable by Faida Ltd. for the year ended 31 December 2006

Date posted: February 26, 2019. Answers (1)

- Primark Ltd. manufactures a variety of goods for the local market. The company commenced operations on 2 January 2006. The following is an extract from...(Solved)

Primark Ltd. manufactures a variety of goods for the local market. The company commenced operations on 2 January 2006. The following is an extract from the company's balance sheet as at 31 December 2006

Required:

i) Capital allowances due to Primark Ltd. for the year ended 31 December 2007.

ii) Tax payable by the company (if any) for the year ended 31 December 2007.

Date posted: February 25, 2019. Answers (1)

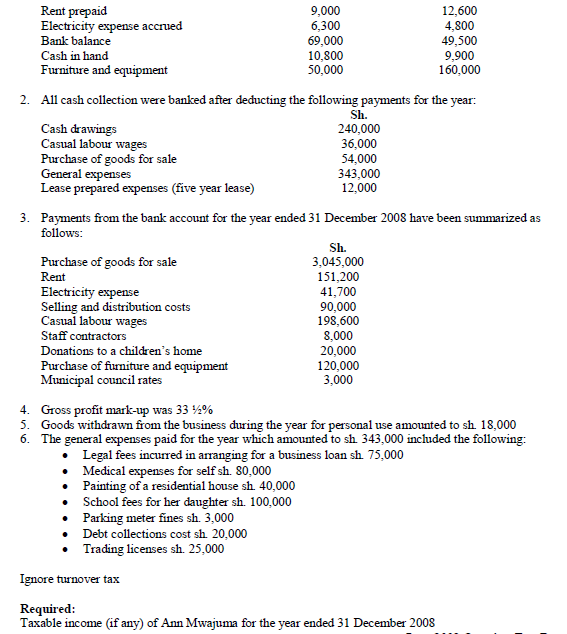

- Ann Mwajuma runs a small business in Kisii town. The revenue authority has asked her to submit a self assessment return for the year ended...(Solved)

Ann Mwajuma runs a small business in Kisii town. The revenue authority has asked her to submit a self assessment return for the year ended 31 December 2008

However, Ann Mwajuma did not maintain complete accounting records for the year ended 31 December 2008. She has therefore requested you to assist her and has provided you with the following information:

1. Opening and closing balances of assets and liabilities were as follows for the year ended 31 December 2008:

Date posted: February 25, 2019. Answers (1)

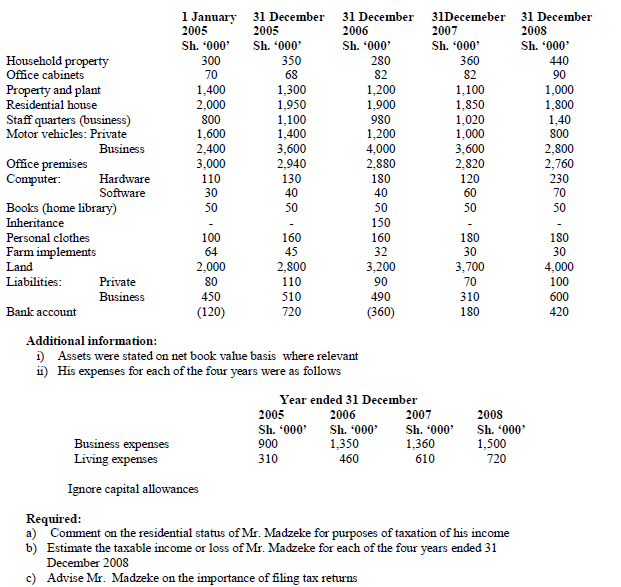

- Mr. Felix Madzeke is a citizen of Malawi but has been residing and conducting business in your country since 2005. However, he was not aware...(Solved)

Mr. Felix Madzeke is a citizen of Malawi but has been residing and conducting business in your country since 2005. However, he was not aware of the requirements to maintain proper records and submitting regular assessment to the revenue authority.

An inspection conducted by the revenue authority on his business and personal transactions over past four years revealed the following:

Assets and liabilities (business and personal) as at:

Date posted: February 25, 2019. Answers (1)

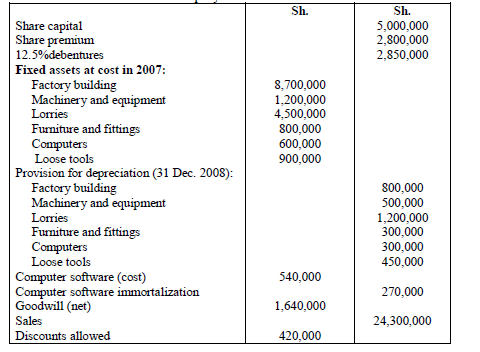

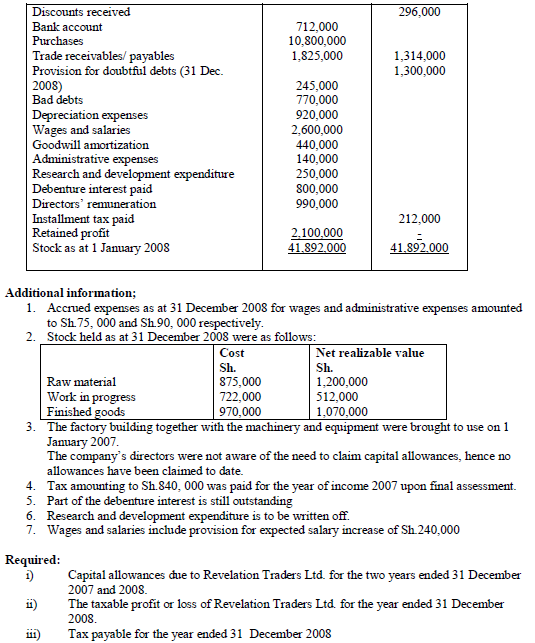

- Revelation Traders Ltd. started its operations on 1 January 2007. The following trial balance was extracted from the books of the company as at 31...(Solved)

Revelation Traders Ltd. started its operations on 1 January 2007. The following trial balance was extracted from the books of the company as at 31 December 2008:

Date posted: February 25, 2019. Answers (1)

- Briefly explain the procedure to be followed when an error on past returns is discovered either by the tax payer or commissioner for Domestic Taxes.(Solved)

Briefly explain the procedure to be followed when an error on past returns is discovered either by the tax payer or commissioner for Domestic Taxes.

Date posted: February 25, 2019. Answers (1)

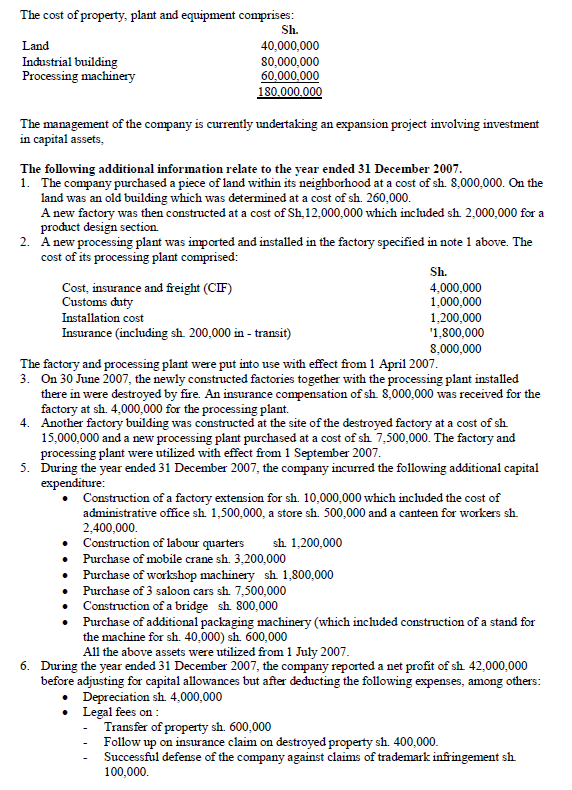

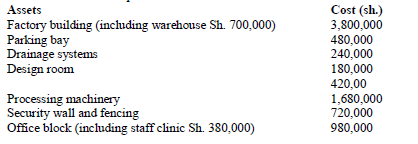

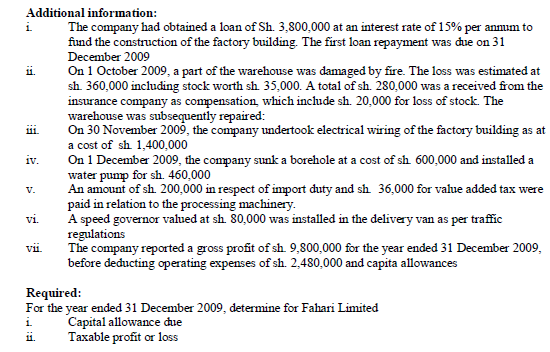

- Fahari Limited, a company making various leather products, commenced operation on 1 January 2009. The following information relate to the assets that the company purchased...(Solved)

Fahari Limited, a company making various leather products, commenced operation on 1 January 2009. The following information relate to the assets that the company purchased or constructed before commencement of operations

Date posted: February 25, 2019. Answers (1)

- What should individuals and corporates put in mind to mitigate their tax exposure or avoid being taxed unfairly?(Solved)

What should individuals and corporates put in mind to mitigate their tax exposure or avoid being taxed unfairly?

Date posted: February 25, 2019. Answers (1)

- How can corporates avoid taxes?(Solved)

How can corporates avoid taxes?

Date posted: February 25, 2019. Answers (1)

- What techniques or ways can individuals take advantage of to avoid taxes?(Solved)

What techniques or ways can individuals take advantage of to avoid taxes?

Date posted: February 25, 2019. Answers (1)

- Tax refunds and tax credits are increasingly being used by governments in the information and modernization taxation policies(Solved)

Tax refunds and tax credits are increasingly being used by governments in the information and modernization taxation policies.

Required:

i) Citing examples distinguish between a tax refund” and a “tax credit”

ii) Evaluate the fundamental role of tax refunds and tax credits in a government’s developments agenda

Date posted: February 25, 2019. Answers (1)

- In the year ended 31 December 2011. Malipo Ltd. earned a profit before tax of Sh. 400 million from its main operation.(Solved)

In the year ended 31 December 2011. Malipo Ltd. earned a profit before tax of Sh. 400 million from its main operation.

In addition, the company earned an investment income of Sh. k60 million. Dividend paid to members for the year amounted to Sh. 98 million.

The corporation tax rate is 30%

Required:

Shortfall tax, inclusive of penalties (if any) payable by the company for the year ended 31 December 2011.

Date posted: February 25, 2019. Answers (1)

- Justify the imposition of shortfall tax on companies(Solved)

Justify the imposition of shortfall tax on companies

Date posted: February 25, 2019. Answers (1)

- A number of countries, particularly in the developing world, have rest fact urea their revenue authorities to provide for large taxpayer units (LTUs).(Solved)

A number of countries, particularly in the developing world, have rest fact urea their revenue authorities to provide for large taxpayer units (LTUs).

Required;

i) Explain three reasons that have motivated the formation of LTUs.

ii) As a tax consultant in a country that intends to form an LTU, describe three key functional areas of an LTU.

Date posted: February 25, 2019. Answers (1)

- Discuss three reasons that related parties may give to justify the continued use of transfer pricing systems.(Solved)

Discuss three reasons that related parties may give to justify the continued use of transfer pricing systems.

Date posted: February 25, 2019. Answers (1)