1. Assets: An asset is a resource controlled by a business entity/firm as a result of past events for which economic benefits are expected to flow to the firm.

An example is if a business sells goods on credit then it has an asset called a debtor. The past event is the sale on credit and the resource is a debtor. This debtor is expected to pay so that economic benefits will flow towards the firm i.e. in form of cash once the customers pays.

Assets are classified into two main types:

i) Non current assets (formerly called fixed assets)-Non current assets are acquired by the business

to assist in earning revenues and not for resale. They are normally expected to be in business for

a period of more than one year.

ii) Current assets-Current assets are not expected to last for more than one year. They are in most

cases directly related to the trading activities of the firm

2. Liabilities: These are obligations of a business as a result of past events settlement of which is expected to result to an economic outflow of amounts from the firm. An example is when a business buys goods on credit, then the firm has a liability called creditor. The past event is the credit purchase and the liability being the creditor the firm will pay cash to the creditor and therefore there is an out flow of cash from the business.

Liabilities are also classified into two main classes.

i) Non-current liabilities (or long term liabilities)-Non-current liabilities are expected to last

or be paid after one year. This includes long-term loans from banks or other financial

institutions.

ii) Current liabilities-Current liabilities last for a period of less than one year and therefore

will be paid within one year.

3. Capital: This is the residual amount on the owner’s interest in the firm after deducting liabilities from the assets.

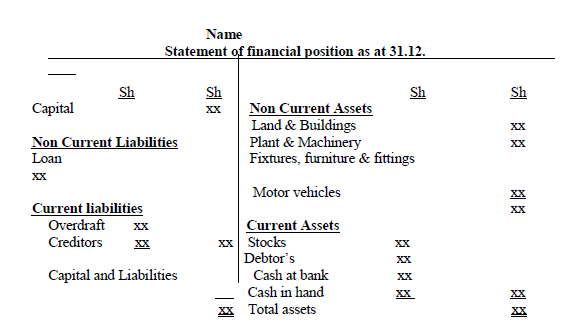

The Accounting equation can be expressed in a simple report called the Statement of financial position (formerly, balance sheet).

The basic format is as follows:

Wilfykil answered the question on

February 28, 2019 at 05:46