-In the general theory, Keynes referred to the speculative motive as part of a

household’s liquidity preferred, since money is the most liquid assets that the

household can hold.

-Depending on the household’s preference between either holding bonds or holding

money, one can construct what has been termed a speculative demand for money

curve for the economy.

-We first need to explore the relationship between the prices of a marketable bond and

the interest rate on that bond because that relationship is fundamental to the

development of a speculative demand for money curve.

-For a simple example we choose a type of bond called a consol, which has no

maturity date or redemption value, but which pays certain number of dollars (R) per

year. The only way of converting the consol into money is for one speculator to sell

to another speculator in the bond market.

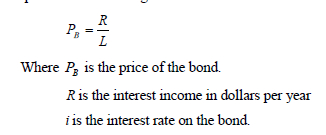

-The price of the bond is given as

There exists an inverse relationship between the price of the bond and the interest rate

on bond. The higher the price of the bond, the lower the interest rate, and vice versa.

Note that the construction of the speculative demand for money curve is based on

fluctuations in the price of bonds and the associated market interest rates.

-The choice between holding idle money balance and holding bonds depends on the

household expectation about the future movement of the market rate of interest.

-Each household would have formed a nation about what it considers the normal rate

of interest (or normal bond price) based on past experiences with the bond market.

-If the actual rate of interest currently varies from the normal rate of interest, the

household would hold the belief that the actual rate of interest will return to the

normal rate of interest in the future.

-If the actual rate of interest (say, 10%) were above the normal rate of interest (say,

8%) the household would expect the actual rate of interest to fall (to 8%) and would

therefore expect the price of bonds to rise.

-In this case the household waiting to make a capital gain would invest in bonds and

would not hold idle speculative money balance.

-However, if the actual rate (say, 6%) were below the normal rate (say,8%) the

household would expect the actual rate (say,6%) to rise to the normal rate.

-In this case, bond prices would fall and the household not wishing to experience a

capital loss on its assets would liquidate its bonds and would hold as an asset would

liquidate its bonds and would hold as an asset in its portfolio only idle speculative

money balance.

-Consider two extreme cases.

Case 1:

actual interest is higher than all the group normal rates of interest.

All groups would certainly expect the price of bond to rise since the price of bond is

currently at its lowest possible level.

All speculators will prefer holding bonds and not speculative money balances.

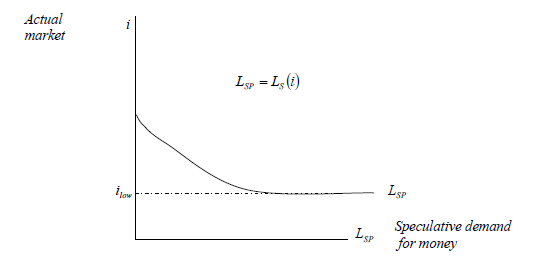

Case 2:

actual rate of interest is at its lowest and below all groups normal rate of interest.

The price of the bond is at its highest and all households that speculate in the bonds

market expects the bonds price to decline in future as actual interest rate rises towards the

normal rate of interest.All household will, therefore, hold idle money balance. In effect there is absolute liquidity.

The absolute liquidity position has been termed a Keynesian liquidity trap

The inverse relationship between actual market rate of interest and the speculative money

demand is presented in the figure below

The liquidated trap is illustrated by the horizontal portion of the speculative demand

for money curve. Note that the liquidity trap would be a phenomenon od a depression

and associated with high level of unemployment.

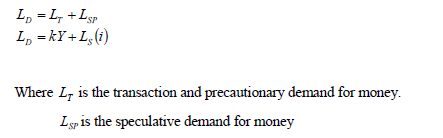

-Keynes’ total demand for money can be expressed as

Thus, the total demand for money depends on the level of income and the market rate

of interest.

sharon kalunda answered the question on

April 11, 2019 at 12:31