(a) Weaknesses of audit at year end

• Number of clients - if the audit firm has a substantial number of clients with similar year

ends, it may be difficult for the auditor to schedule his/her staff to cover all the clients

• Size of a company - it might not be possible to carry out an audit of a large

firm/company comprehensively.

• Increases auditor's liability - it might increase the liability of the auditor especially if

the sample tested is small.

• Delays the annual general meeting - in case of unforeseen circumstances, final audits

could take a significant amount of time and thus delaying the reports necessary to

convene an annual general meeting, especially where the internal controls are weak.

• Errors and frauds - the errors and frauds detected at the year-end could be enormous for

a firm/company to contain.

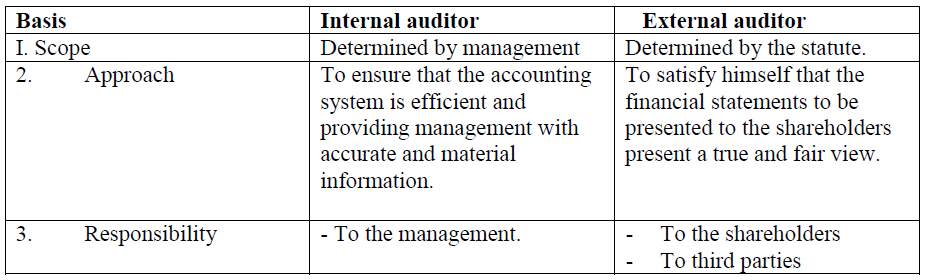

(b) Fundamental differences between internal and external auditors:

l

Kavungya answered the question on

May 14, 2019 at 12:32