i) Risk adjusted discounting rate – This technique is used to establish the discounting rate to be used for a given project. The cost of capital of the firm will be used as the discounting rate for a given project if project risk is equal to business risk of the firm. If a project has a higher risk than the business risk of the firm, then a percentage risk premium is added to the cost of capital to determine the discounting rate i.e.discounting rate for a high risk project = cost of capital + percentage risk premium. Therefore a high risk project will be evaluated at a higher discounting rate.

ii) Market Model – This model is used to establish the percentage cost of ordinary share capital cost of equity (Ke). If an investor is holding ordinary shares, he can receive returns in 2 forms:

- Dividends

- Capital gains

Capital gain is assumed to constitute the difference between the buying price of a share at the beginning of the (P

0), the selling price of the same share at the end of the period (P

1). Therefore total returns = DPS + Capital gains = DPS + P

1 – P

0.

The amount invested to derive the returns is equal to the buying price at the beginning of the period (P

0) therefore percentage return/yield =

iii) Capital asset pricing model (CAPM)

iii) Capital asset pricing model (CAPM) – CAPM is a technique that is used to establish the required rate of return of an investment given a particular level of risk. According to CAPM, the total business risk of the firm can be divided into 2:

a) Systematic Risk – This is the risk that affects all the firms in the market. This risk cannot be eliminated/diversified. It is thus called undiversifiable risk. Since it affects all the firms in the market, the share price and profitability of the firms will be moving in the same direction i.e. systematically. Examples of systematic risk are political instability, inflation, power crisis in the economy, power rationing, natural calamities – floods and earthquakes, increase in corporate tax rates and personal tax rates, etc. Systematic risk is measured by a Beta factor.

b) Unsystematic risk – This risk affects only one firm in the market but not other firms. It is therefore unique to the firm thus unsystematic trend in profitability of the firm relative to the profitability trend of other firms in the market. The risk is caused by factors unique to the firm such as:

- Labour strikes by employees of the firm;

- Exit of a prominent corporate personality;

- Collapse of marketing and advertising programs of the firm on launching of a new product;

- Failure to make a research and development breakthrough by the firm, etc

CAPM is only concerned with systematic risk. According to the model, the required rate of return will be highly influenced by the Beta factor of each investment. This is in addition to the excess returns an investor derives by undertaking additional risk e.g cost of equity should be equal to R

f + (R

m – R

f)B

ECost of debt =R

f + (R

m – R

f)B

dWhere:

R

f = rate of return/interest rate on riskless investment e.g T. bills

R

m = Average rate of return for the entire stock as shown by average Percentage return of the firms that constitute the stock index.

B

E = Beta factor of investment in ordinary shares/equity.

B

d = Beta factor for investment in debentures/long term debt capital.

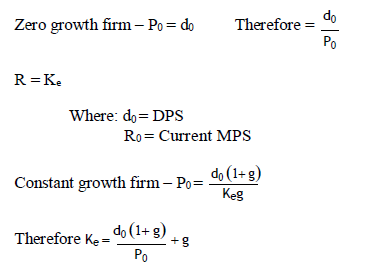

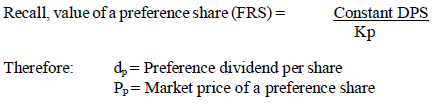

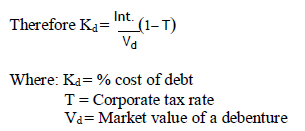

iv) Dividend yield/Gordon’s Model – This model is used to determine the cost of various capital

components in particular:

- Cost of equity - K

e- Cost of preference share capital (perpetual) – K

p- Cost of perpetual debentures – K

da) Cost of equity (K

e)– This can be determined with respect to:

b) Cost of perpetual preference share capital (K

p)

c) Cost of perpetual debenture (K

d) – Debentures pay interest charges, which an allowable expenses for tax purposes.

Wilfykil answered the question on

August 5, 2019 at 06:11