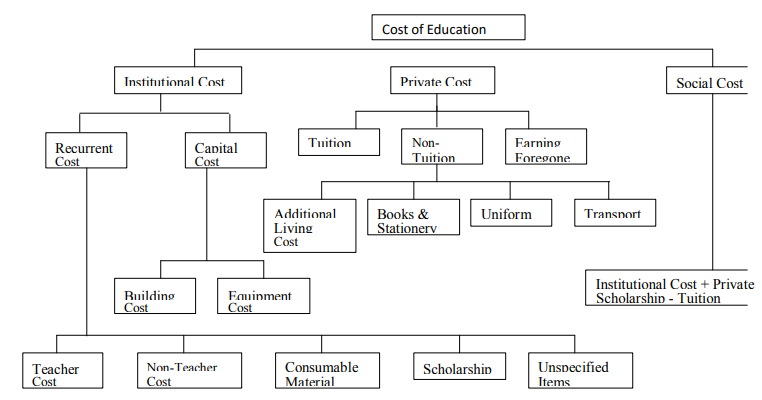

Costs can be classified into two types :

- Individual or Private Costs

- Institutional or Public or Social Costs

- Direct Costs

- Indirect Costs

- Opportunity Costs

(a) Individual Costs or Private Cost: Individual costs or private costs of education are those costs of education incurred by a learner or by his/her parents/guardians or by the family as a whole.

These concern individuals in families and represent costs which the individuals and the families must bear in return for the education received. Individual costs are of two types: direct and indirect.

Examples of private costs are as follows : Tuition and examination fees and other such fees, institutional supplies, manuals and books, transport, uniforms and foregone earnings.

b) Institutional/Public/Social Costs : These costs concern society and refer to such costs (or expenditure) as are borne out as a result of all education and training activities in a society at a given point of time. Costs incurred at the institutional level (government, private or mixed) are called institutional costs or public costs of education. Public costs are those that include financing by the government on the basis of taxes, loans and other public revenues. The

institutional costs of education are, generally, analysed in terms of;

Variable and fixed costs of education, Recurring and non-recurring costs of education and

Current and capital costs of education. Institutional/Public/Social costs are also of two types: direct and indirect.

(c) Direct Costs: These are those costs that are directly visible. They include all money expenditure incurred on different items by the student. Direct costs are expenses that can be separately identified and charged as part of the cost of a product, service, or department. Typical direct costs include items such as instructional and other programme materials printed, fuel, oil and repairs of vehicles used for home-to-school transportation, centralised data processing services, in-house equipment repairs, field trips, expenditure on tuition fees, other fees and charges, purchase of

books, stationary, uniforms, hostel expenses and transport.

(d) Indirect Costs : Indirect costs are those costs that cannot be directly charged to a particular programme, but are attributed to services, which are necessary to operate the program. Such services include, but are not limited to, accounting, budgeting, payroll preparation, personnel management, and purchasing, warehousing and centralised data processing. Some programs cap the allowed indirect cost rates, others have an administrative cap that limits a combination of direct administrative costs and indirect costs, while others do not allow indirect costs at all, requiring

that the entire award amount be spent on direct costs. These expenses are not paid directly to your school, but are associated with attending school. You and your family can control some of them.

(e) Opportunity Cost: Opportunity cost is a concept you did not see in the definition of economics. But not seeing it doesn’t mean that it isn’t there. There is yet more to say about the definition, but this is the logical place to introduce a related concept. Opportunity costs are everywhere, due to scarcity and the necessity of choosing. Opportunity cost is not what you choose when you make a choice -it is what you did not choose in making a choice. Opportunity cost is the value of the forgone alternative - what you gave up when you got something. The opportunity cost of going to college is the money you would have earned if you worked instead. On the one hand, you lose four years of salary while getting your degree; on the other hand, you hope to earn more during your career, due to your education, to

offset the lost wages. Thus, opportunity cost is the cost of alternatives foregone.

raphael answered the question on

August 4, 2021 at 07:28