1. Classification of Costs for Decision Making, Planning and Control

(a) According to cost behaviour

According to the variability with the level of activity (volume) we have fixed, mixed and variable costs.

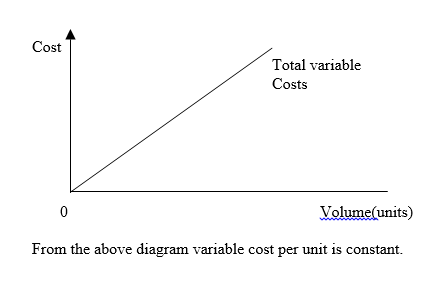

(i) Variable costs

A cost that changes in total in direct proportion to changes in the related activity level or volume e.g cost of material, sales commission, purchase cost. Diagrammatically these can be shown as below:

2. According to the degree of traceability to the final product:

By looking at the final product, one can see the production costs e.g. management cost of a chalk.

We have direct and indirect costs.

(i) Direct Costs ( also prime costs)

Costs that can be valued in total to the product or service that is being costed e.g. direct material costs, direct labour costs and direct expenses.

Prime cost = direct expenses + direct labour + direct expenses

(ii) Indirect costs (Overhead costs)

Costs which in the process of making a product or providing a service or running a department but which cannot be traced directly and in full to the product, service or department e.g. indirect materials, indirect labour, indirect expenses such as cost of utilities, stationery, supervisory, salaries etc.

Overheads = indirect material + indirect labour + indirect expenses

Total cost of production = prime costs + overheads

Conversion costs = Total costs – material costs

Convention cost is cost of converting input material into final product.

3. According to the relevance:

We have relevant costs and irrelevant costs.

(i) Relevant Costs:

Cost which can change the decision under consideration.

(ii) Irrelevant costs:

Costs which if changed will not affect the decision under consideration.

To be relevant a cost must:

(i) Relate to the future - historical costs are not relevant.

(ii) Be incremental (differ between cost with decision and cost what decision)

(iii) Be Cash flow in nature - costs which do not affect cost inflows and outflows e.g. depreciation, notional (imputed) rent/interest etc.

4. Avoidable or Unavoidable

According to what degree costs can be avoided we have:

(i) Avoidable costs:

Cost saved by not adopting a given alternative.

(ii) Unavoidable costs:

These are costs that will be incurred regardless of whether the decision is made or not.

Avoidable costs are relevant for decision-making. Unavoidable costs are irrelevant for decision- making

Opportunity Cost

Measures the opportunity foregone or sacrifice made when the choice of the action requires an alternative action to be given up. It relates to the use of scarce resources.

(a) Classification by function or department. Costs can be classified either as manufacturing, sales and marketing, Research & Development costs etc.

(i) Manufacturing costs: (Production costs)

These are costs incurred by the sequence of operation beginning with the supplier of raw materials and ending with the completion of the product ready for warehousing (inputs to finished goods).

(ii) Administration costs

These are costs of managing an organization i.e. costs of planning and controlling company operations e.g. management salaries.

(iii) Sales and marketing costs

These are costs of creating demand for the product and securing firm orders from the customers.

(iv) Distribution costs

These are costs of sequence of operations beginning with the receipt of finished goods from production department and ending with the reconditioning for re-use of returned empty containers.

(v) Research and Development costs

These are costs of searching for new or improved products and costs of producing such products.

Other costs

(i) Discretionary and Non-discretionary costs

Discretionary costs These are costs where managers make decisions to incur or not. These relate to support services e.g. advertising costs

Non discretionary costs: must be incurred you cannot choose not to incur material costs for production to take place.

(ii) Committed costs

These are costs that have not been incurred but have been planned to be incurred e.g. a contract. They are irrelevant costs.

(iii) Sunk costs

Historical costs that have no future benefits. Have already been incurred or paid for. They are not relevant for decision making.

Titany answered the question on

October 12, 2021 at 05:35